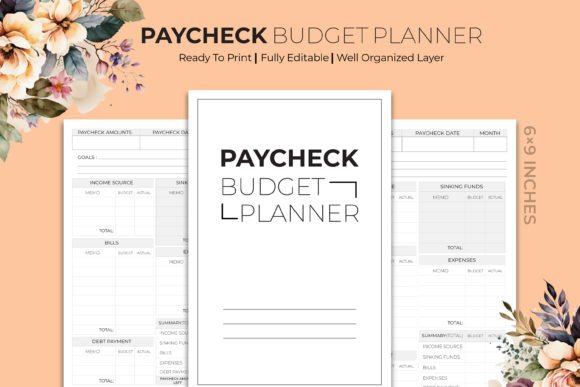

The Paycheck Budget KDP Planner Interior: A Flexible Framework for Intentional Spending

Most budgets fail because they treat income as a single monthly lump. That approach ignores the reality of when money actually arrives—and how quickly it can vanish between bills, variable expenses, and the unexpected. A Paycheck Budget KDP Planner Interior shifts the focus from a calendar month to each individual pay period, making money feel more manageable and less abstract. It’s not just another spreadsheet. It’s a fully designed, printable toolkit that can be used as-is or customized, printed, and even sold as a physical product through Amazon KDP.

Why a Paycheck-by-Paycheck Approach Changes Everything

Traditional budgeting often asks you to project a whole month’s income and then assign every dollar, but that’s hard when you’re paid biweekly or weekly. The gap between your rent due date and your second paycheck can create a sense of scarcity even when the math works out on paper. A paycheck planner breaks the month into smaller, more predictable chunks. You assign a specific job to every dollar from that single check before the next one lands.

This method is especially powerful for anyone with irregular cash flow. A server whose tips fluctuate, a freelancer juggling multiple clients with different payment schedules, or a small business owner paying themselves from sporadic revenue all find more clarity when they budget per check rather than per month. The planner gives each deposit its own mini-budget: first cover immediate obligations, then allocate for upcoming bills, then decide what can go toward sinking funds or flexible spending. It turns a guessing game into a repeatable rhythm.

Who Really Benefits from a Ready-Made Planner Interior

The beauty of this type of interior isn’t limited to one kind of user. Different people encounter the Paycheck Budget KDP Planner Interior for vastly different reasons, and each discovers unique advantages.

Freelancers and Independent Contractors

Unpredictable income is the norm. A graphic designer might receive three payments in one week and nothing for the next two. Rather than averaging income across a month, a paycheck budget lets them tackle each deposit as it arrives. They can immediately assign portions to taxes, business expenses, and personal bills in proportion, making sure a “good week” doesn’t lead to overspending that hurts later. Because the designer can print as many sheets as needed, the planner never runs out of room.

The Side Hustle Generation

Someone working a full-time job while driving for a rideshare or selling handmade items often struggles to separate primary income from side income. A physical planner gives each income stream its own space. The main paycheck budget handles core expenses; the side hustle check gets its own planner page dedicated to debt payoff, savings goals, or reinvesting in the business. This visual separation reduces mental load and makes progress visible.

Couples Merging Finances

Different pay schedules can create friction. One partner might be paid on the 1st and 15th, the other every Friday. Using a shared planner or sitting down with individual pages helps both see exactly what’s covered and what needs to wait. It turns financial conversations from vague worries into concrete, collaborative planning sessions. Because the interior is editable, a couple can adapt categories—like renaming a section to “Joint Vacation Fund” or “Pet Emergency.”

Coaches and Financial Educators

Money coaches often need a simple, reliable tool they can hand to clients without overwhelming them with apps or complex spreadsheets. A printable paycheck budget becomes a homework tool. The coach might customize it with their branding, add a note section for action items, and give clients something tactile to work through between sessions. Since the planner interior is fully vector and scalable, it can be reformatted for different teaching formats or bound into a workbook.

Adapting the Same Planner to Different Lifestyles

One of the most underrated strengths of a fully editable interior is how it morphs to fit entirely different needs. A minimalist single person will use it differently than a parent of three. A digital nomad traveling across time zones might print a few sheets at a time, keeping only what’s immediately relevant. Someone deeply focused on environmental impact might reduce the number of printed pages and rotate digital copies, using the high-resolution files on a tablet.

Because the design comes with 100 unique templates, users aren’t locked into a single layout. A student might grab a simpler version that focuses on essential bills and a small “fun” allocation. A family might choose a more detailed version with columns for grocery, medication, childcare, and seasonal events. The Paycheck Budget KDP Planner Interior doesn’t force one rigid system; it offers a starting framework that can be selected and tweaked to match exactly how someone thinks about their money.

Why Physical Planners Still Win Over Apps

Digital tools are everywhere, yet a surprising number of people still prefer paper for money matters. Writing down numbers engages different cognitive processes. It slows down the mind enough to catch mistakes or spot patterns that scrolling never reveals. A printed planner can sit on a desk as a gentle reminder, while an app can be ignored with a swipe. There’s also no distraction: no notifications, no syncing issues, no battery anxiety. For many, the privacy of paper is a relief.

For creators who intend to sell on Amazon KDP, this preference is a real market signal. Buyers seek out paper planners because they want that physical experience. When the interior is already formatted to 6x9 inches, with no-bleed setup and rigorously Amazon-tested for upload errors, the technical barriers vanish. The seller can focus on cover design and marketing, knowing the inside structure works flawlessly.

Common Scenarios Where a Paycheck Planner Shines

- Starting a Debt Snowball: Assigning extra payments from a specific paycheck keeps momentum without over-committing from a single large deposit. It feels safer to say, “From my second check this month, $200 goes to the smallest balance.”

- Building a Mini Emergency Fund: Instead of aiming for a huge goal all at once, a user might decide that 5% of every check goes into a cushion. Over time, that becomes a number large enough to handle a sudden car repair.

- Managing Seasonal Work: Someone in construction or tourism often has feast-or-famine cycles. During high-income months, the planner helps allocate a set amount to “off-season living” so the lean months don’t feel panicked.

- Planning for Irregular Large Expenses: An annual insurance premium or a holiday spending spree can be broken down into per-paycheck chunks. Setting aside $45 from each check over six months feels almost invisible but fully funds the cost.

Each of these scenarios uses the same core idea—budgeting per check—but the emotional weight shifts from dread to control. The planner becomes a record of small, consistent decisions rather than a rigid set of rules.

Things to Consider Before Using or Selling a KDP Planner Interior

No tool is perfect for everyone. Paper planners require consistency. Someone who never looks at physical pages won’t magically adopt a weekly habit; they might need a transition period where they also use a phone reminder. The template itself demands a bit of honesty: if someone isn’t ready to face their true spending, no layout can fix that.

For those planning to sell the planner, it’s worth noting that the market for budget journals is competitive. Standing out requires a clear understanding of who the end user is—maybe it’s new parents, recent graduates, or people recovering from a financial setback. The Paycheck Budget KDP Planner Interior makes customization straightforward because everything from color to font to section labels is editable, but that also means the seller must put thought into how they tailor the message. The files are fully vector and 300 DPI, so enlarging or tweaking any element for a different cover style or promotional image won’t degrade quality. The included Adobe Illustrator, EPS, and PDF formats give flexibility depending on the creator’s software skills.

One limitation to keep in mind is that not all users are comfortable editing vector files. While the interior is scalable and editable, a potential seller who doesn’t have basic Illustrator knowledge may need to learn a few simple skills or stick to the ready-to-print PDF version as is. Even then, the 100 unique design templates provide enough variety that many will find a layout that fits without any extra editing.

Making the Planner Feel Like Yours

Whether using it personally or building a brand around it, the ability to change text, colors, and design elements matters. A wellness coach might add a section for “Money Mindset Check-In.” A frugal living blogger could insert a small spending tracker with icons. A parent teaching teens about money might simplify categories even further and bump up the font size. None of these tweaks requires starting from scratch, because the bones of the paycheck budget method are already there, cleanly structured.

The interior’s no-bleed format and strict 6x9 sizing also mean it plays well with print-on-demand services beyond Amazon. It can be sent to a local print shop for a spiral-bound version or used as a digital download in an Etsy shop. Because it’s Amazon-tested, the frustrating back-and-forth of file rejections gets minimized—a real time-saver for anyone who has ever wrestled with KDP’s upload requirements.

Why the Paycheck Budget Method Sticks

The reason so many people abandon complicated budgeting software is that those systems ask for too much maintenance. A paycheck budget, paired with a thoughtfully designed interior, asks only that you show up when money arrives. That frequency—every week or two—creates a natural check-in that feels less like a chore and more like a quick habit. Over time, users begin to internalize their numbers. They start to know without looking what portion of each check goes to rent, what’s left for groceries, and exactly how much freedom they have. That’s when anxiety drops and real, lasting confidence grows.

For the adult who feels behind or out of control, a physical planner sometimes becomes the first thing they genuinely keep up with. For the entrepreneur, it can become a low-maintenance product that helps others while generating passive income. The Paycheck Budget KDP Planner Interior isn’t a magic solution, but it’s a practical, flexible starting point that respects the way money actually moves through a real person’s life—one check at a time.